Index Funds: The foundation for long‑term portfolios

Index funds offer one of the simplest and most effective ways for investors to participate in the stock market without stress, guesswork, or constant monitoring. Over time, they have proven to be an ideal foundation for building resilient, well balanced - portfolios.

JioBlackRock advantage

·

Published on 2 April 2026

·

4 min read

What exactly is an index fund?

Unlike actively managed funds, where a fund manager selects stocks, changes allocations, and takes active calls in an attempt to outperform their respective benchmark — index funds follow a rules ‑based and predictable approach. The fund simply holds the same stocks and in the same proportion as the index.

To make index funds more stringent and compliant, SEBI regulations require index funds to invest at least 95% of their assets in the same securities (and in the same proportions) as the index they track. When the index rises, the fund rises. When it falls, the fund falls. This transparency makes index funds easy to understand and easier to stick with through market ups and downs.

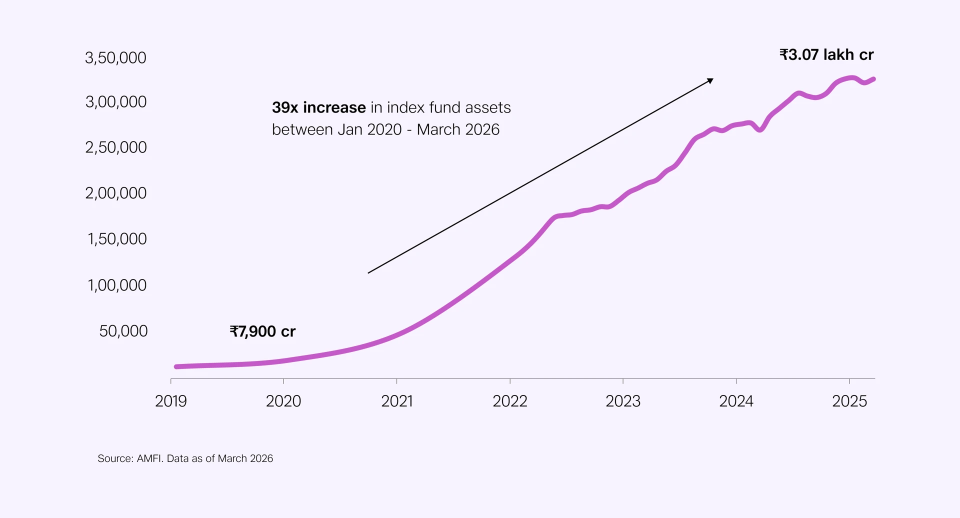

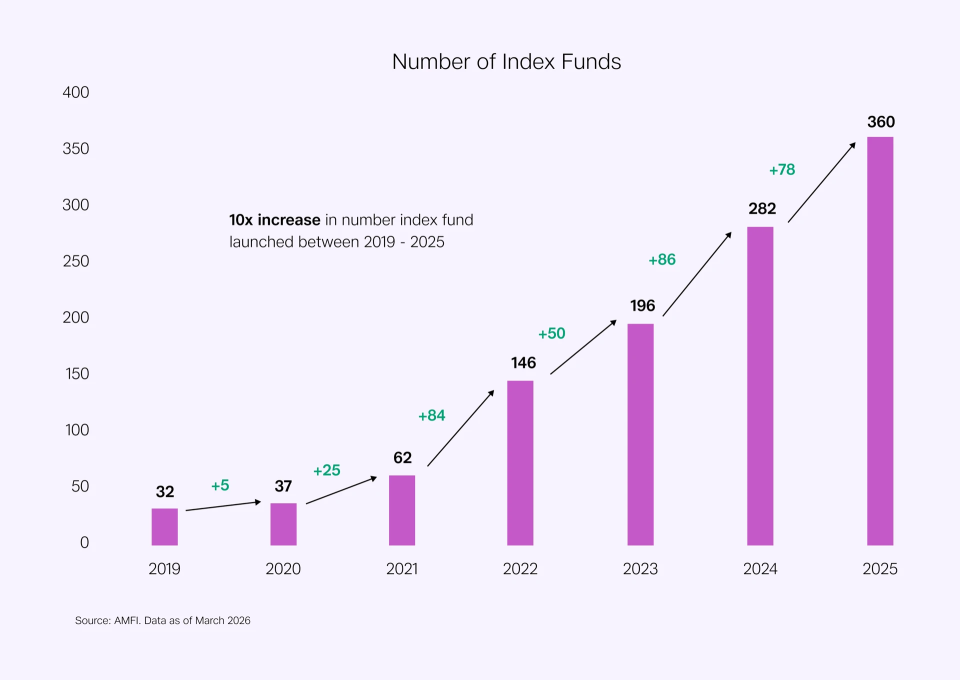

The data tells a clear story: index funds are gaining ground

Index fund assets have grown from ₹7,900 crore in January 2020 to ₹3.24 lakh crore by February 2026, a remarkable 41x increase.

Source: AMFI. Data as of February 2026

Source: AMFI. Data as of February 2026

This surge reflects increasing investor confidence in index funds. The reasons are both simple and compelling:

1. Predictability:

Index funds deliver market linked returns. Investors know exactly what they own and what returns to expect relative‑ to the market. For example, if you want exposure to the large-cap segment in India, a large-cap index fund allows you to capture the overall large-cap market movement efficiently, without depending on a fund manager’s stock-picking skills or biases.

2. Low cost:

With no active stock selection or frequent churn, index funds come with very low expense ratios (can be as low as for e.g. 0.05%). Lower costs mean more of your money stays invested, allowing compounding to work more efficiently over the long term.

3. Diversification:

By tracking broad indices, index funds offer diversification across companies and sectors. This reduces the risk of over‑reliance on a few stocks or themes and helps smoothen portfolio volatility.

Together, these three factors make index funds a powerful core holding for long‑term investors

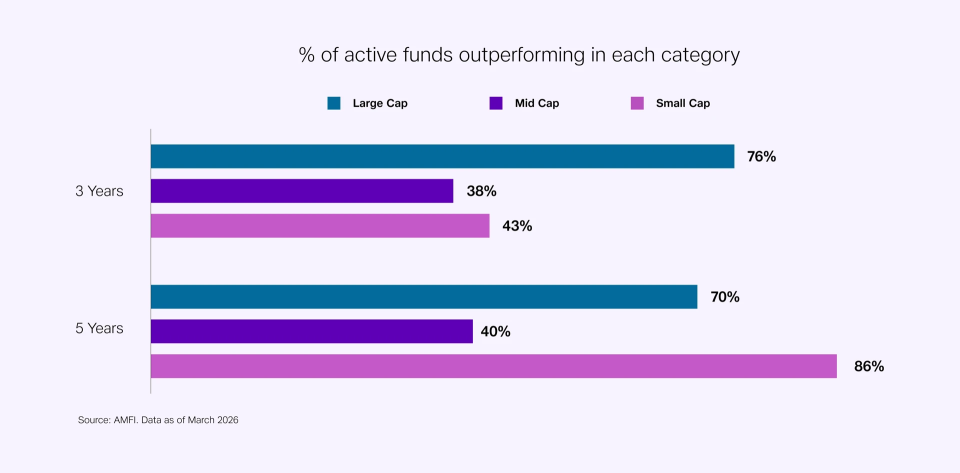

How index funds fit into the performance landscape

For instance, many investors believe that active management should work better in the mid- and small-cap space, actual outcomes tell a more nuanced story.

In the midcap and smallcap segments, allocation to passive funds (which include index funds and ETFs) remains extremely low, at just 4% in mid caps and 3% in small caps (AMFI. Data as of February 2026). Many investors believe that these segments offer greater inefficiencies and, therefore, better opportunities for skilled fund managers to generate alpha. As a result, active funds continue to dominate investor allocations in these categories.

However, actual performance outcomes challenge this belief. Over the last three years, only 38% of active midcap funds and 25% of active smallcap funds have outperformed their respective market benchmarks (AMFI, Data as of February 2026). In other words, even in segments where active management is expected to shine, consistent outperformance has been difficult and highly unpredictable.

In contrast, in the ‑largecap space, passive funds (index funds and ETFs) account for nearly 65% of large-cap exposure (AMFI. Data as of February 2026), reflecting growing confidence in passive investing. This is mainly because large companies are well researched and information about them is easy to find, leaving little room to earn extra returns. As a result, low-cost passive funds that track the market are often seen as a smart and efficient choice.

Interestingly, performance data shows that about 73% of active largecap‑ funds have managed to outperform their benchmarks over the last three years (AMFI, Data as of February 2026).

Source: AMFI. Data as of February 2026

This gap between expectations and outcomes highlights a key reality of investing. While active funds can outperform in certain periods, keeping track of those winners in advance — and staying invested through inevitable phases of underperformance is far from easy. Many investors end up redeeming funds at the wrong time, eroding returns in the process.

Index funds don’t rely on manager skill or timing decisions. Instead, they ensure steady participation in the market’s growth, making them especially effective as a core portfolio holding within a long-term portfolio, and providing you an opportunity to diverse your portfolio.

Bottom line: Ideal foundation for long‑term portfolios

Start simple. Stay disciplined. And let the power of the market work for you.

Disclaimer: This article is for educational purposes only.

Blogs

We want everyone to feel confident about investing and our learning hub is a good place to start – wherever you are on your journey.

From Products to Purpose: Why a Personalised Investment Plan Matters

Owning financial products or even having a portfolio may not be enough. What you really need is a Personalised Investment Plan. Read more to understand why.

What you miss out without personalised investment advice

Investing is a life step that is too important to leave to chance. Using a professional adviser for personalised advice is the key to meeting your investment objectives.

Smart investing for women: Build wealth your way

This article reveals how women can take charge of their wealth with investment strategies tailored to their unique life journeys.

Is your portfolio over-diversified? How to achieve the right balance

Diversification is key, but too much of it can affect your returns. Learn how to strike the right balance and build a portfolio that’s tailored to you.

Appointing nominees: a guide for investors

A nominee is someone you appoint to act as a custodian of your financial assets in the event of your death. They will be responsible for transferring the proceeds of your investments to your heirs. This guide explains what you need to know about nominees, how to appoint them and why it matters. Appointing a nominee does not transfer ownership of your assets while you are alive: it is a legal mechanism that ensures the smooth transfer of funds in the event of your death.

Smart SIPs from JioBlackRock: Redefining the way investors build wealth

Discover how Smart SIPs will transform normal investing into a dynamic, intelligent strategy. Learn why this dynamic and personalised approach could be the right move for your financial future.