Monthly Asset Allocation View - March 2026

What's shaping markets this March? The JioBlackRock Investment Team shares our March Asset Allocation Commentary, explaining recent market movements and how portfolios are being positioned today. Explore our latest market views and asset allocation insights in the note below.

Published on 21 March 2026

·

2 min read

Market Review

Cricket is a religion in India, and it truly brings the country together. There were lots of life learnings from India’s recent T20 World Cup victory and there were some similarities with investing too. From having a long-term strategy to making timely tactical changes, to have the right balance for the team to providing role clarity, diversification and simple execution. All these things equally apply to how investors can manage their investment portfolios.

Last few weeks highlighted the importance of discipline, diversification and clear strategy again as equity markets experienced heightened volatility due to the US, Israel and Iran conflict. Historically, such events have triggered short-term volatility, with oil prices moving higher and investor sentiment turning cautious before the situation eventually stabilizes. Conditions currently remain fluid and disruptions in Strait of Hormuz are causing significant challenges in the delivery of oil and gas globally.

India and US progressed on a trade deal in early February. However, the initial positive reaction got subdued by heightened global geopolitical risk. Benchmark equity indices traded largely sideways in February but have moved down in March with broad based weakness. Across sectors, IT indices saw sharp declines on fears of AI-led global disruption for software companies.

The December quarter earnings season delivered healthy profit growth across sectors, underscoring improving outlook in India’s corporate earnings cycle. Nifty 500 companies delivered strong double-digit sales growth in the December quarter, the highest in ten quarters, but earnings growth was the lowest in the last five quarters. Aggregate earnings and sales of the Nifty 500 universe grew by 9% YoY and 13% YoY respectively. The earnings performance of the Nifty 500 was supported by mid- and small-cap companies where aggregate earnings grew 20% YoY and 13% YoY respectively, whereas the large-cap companies grew at 7% YoY.

India’s macroeconomic fundamentals were strong. Headline CPI inflation for January 2026 stood at 2.75% YoY and the Reserve Bank of India (RBI) raised its FY26 real Gross Domestic Product (GDP) growth forecast to 7.4%, supported by resilient private consumption, sustained government capital expenditure, healthy credit growth, and improving corporate balance sheets. The central bank highlighted continued momentum in services, a recovery in manufacturing activity, and robust investment conditions as key drivers of domestic demand. The recent spike in crude oil prices introduces a new source of uncertainty and will need to be monitored closely.

From Indian economy perspective, consensus estimate from economists highlights that a USD 10 per barrel sustained increase in crude oil prices could lower India’s GDP growth by ~20–25 basis points and widen the current account deficit by ~0.4% of GDP, while also exerting upward pressure on inflation and bond yields.

Last few weeks highlighted the importance of discipline, diversification and clear strategy again as equity markets experienced heightened volatility due to the US, Israel and Iran conflict. Historically, such events have triggered short-term volatility, with oil prices moving higher and investor sentiment turning cautious before the situation eventually stabilizes. Conditions currently remain fluid and disruptions in Strait of Hormuz are causing significant challenges in the delivery of oil and gas globally.

India and US progressed on a trade deal in early February. However, the initial positive reaction got subdued by heightened global geopolitical risk. Benchmark equity indices traded largely sideways in February but have moved down in March with broad based weakness. Across sectors, IT indices saw sharp declines on fears of AI-led global disruption for software companies.

The December quarter earnings season delivered healthy profit growth across sectors, underscoring improving outlook in India’s corporate earnings cycle. Nifty 500 companies delivered strong double-digit sales growth in the December quarter, the highest in ten quarters, but earnings growth was the lowest in the last five quarters. Aggregate earnings and sales of the Nifty 500 universe grew by 9% YoY and 13% YoY respectively. The earnings performance of the Nifty 500 was supported by mid- and small-cap companies where aggregate earnings grew 20% YoY and 13% YoY respectively, whereas the large-cap companies grew at 7% YoY.

India’s macroeconomic fundamentals were strong. Headline CPI inflation for January 2026 stood at 2.75% YoY and the Reserve Bank of India (RBI) raised its FY26 real Gross Domestic Product (GDP) growth forecast to 7.4%, supported by resilient private consumption, sustained government capital expenditure, healthy credit growth, and improving corporate balance sheets. The central bank highlighted continued momentum in services, a recovery in manufacturing activity, and robust investment conditions as key drivers of domestic demand. The recent spike in crude oil prices introduces a new source of uncertainty and will need to be monitored closely.

From Indian economy perspective, consensus estimate from economists highlights that a USD 10 per barrel sustained increase in crude oil prices could lower India’s GDP growth by ~20–25 basis points and widen the current account deficit by ~0.4% of GDP, while also exerting upward pressure on inflation and bond yields.

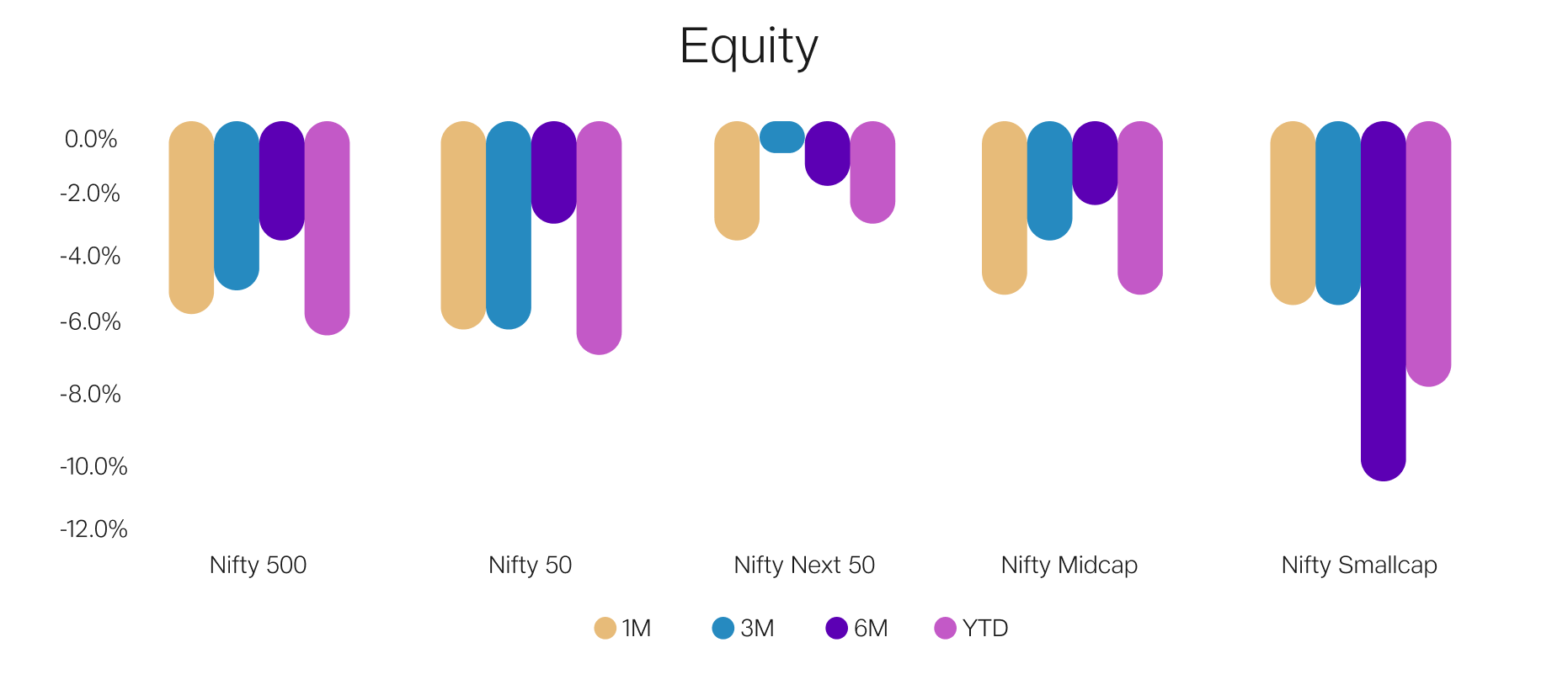

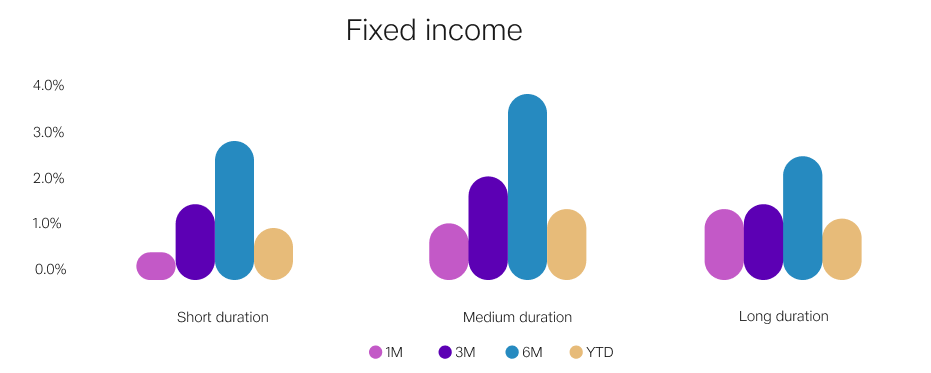

Market Performance

Source: Bloomberg,

Data: As of 10th March 2026

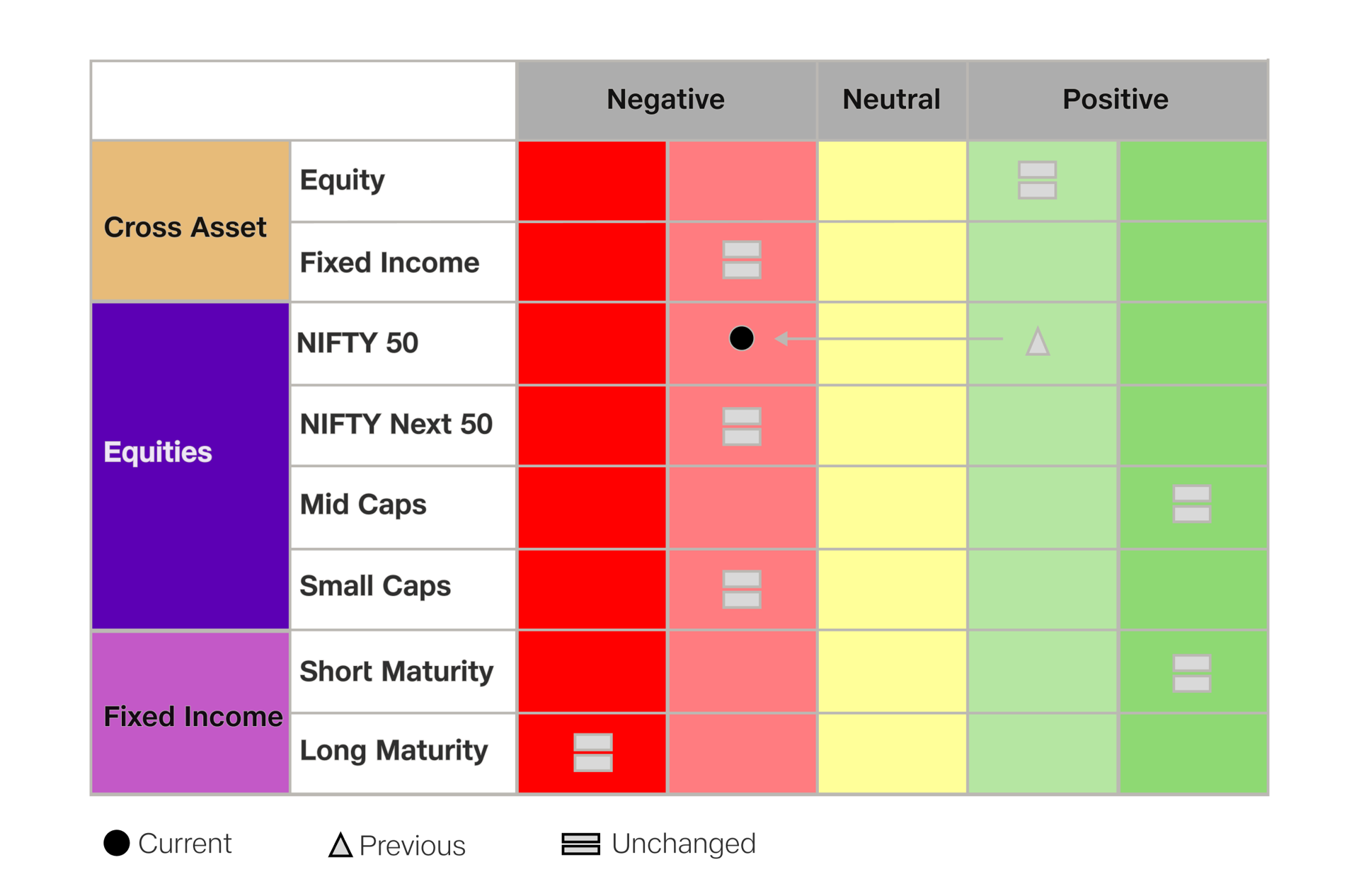

Asset Allocation View

We continue to view equities favourably, supported by a combination of improved valuations on back of broad-based improvement in earnings momentum and supportive growth conditions. While near‑term volatility has increased due to global geopolitical developments, we see this as an opportunity to increase exposure to equities from a longer-term perspective. Long-term structural story for India remains intact.

Within equities, our preference for mid‑cap companies continues as their earnings expectations continue to move higher. Although valuations across parts of the mid‑cap universe remain above long‑term averages, the strength and breadth of earnings growth provide support.

At the same time, we maintain a modest tactical underweight to large‑cap and small- cap companies. While large-caps continue to offer balance sheet strength and stability in volatile phases, relative earnings momentum has been stronger in the mid-cap companies. In addition, select large‑cap segments remain more exposed to global growth uncertainties and currency‑related volatility, warranting a cautious stance.

From a macro perspective, expectations for further policy rate cuts have moderated. However, the monetary policy remains focused on maintaining adequate liquidity and supporting growth. Within fixed income, current conditions reinforce our preference for shorter‑duration strategies, where carry remains attractive and exposure to volatility is relatively contained.

Our current asset allocation signals:

Disclaimer for Monthly Asset Allocation Commentary.

Within equities, our preference for mid‑cap companies continues as their earnings expectations continue to move higher. Although valuations across parts of the mid‑cap universe remain above long‑term averages, the strength and breadth of earnings growth provide support.

At the same time, we maintain a modest tactical underweight to large‑cap and small- cap companies. While large-caps continue to offer balance sheet strength and stability in volatile phases, relative earnings momentum has been stronger in the mid-cap companies. In addition, select large‑cap segments remain more exposed to global growth uncertainties and currency‑related volatility, warranting a cautious stance.

From a macro perspective, expectations for further policy rate cuts have moderated. However, the monetary policy remains focused on maintaining adequate liquidity and supporting growth. Within fixed income, current conditions reinforce our preference for shorter‑duration strategies, where carry remains attractive and exposure to volatility is relatively contained.

Our current asset allocation signals:

| Category | Summary |

|---|---|

| Macro | The policy easing cycle is behind us, but macro conditions remain supportive. With inflation still benign, the RBI’s focus has shifted to maintaining liquidity, managing external shocks (oil, currency), and supporting growth. |

| Sentiment | Market sentiment has turned more cautious but is still not outright negative. Domestic investors continue to provide support despite outflows from foreign investors. |

| Fundamentals | Earnings momentum has improved and is broad-based. A large share of companies reported double-digit profit growth and positive surprises. |

| Valuation | Valuations have improved from previously elevated levels and are providing opportunities in select segments. |

Disclaimer for Monthly Asset Allocation Commentary.

Blogs

We want everyone to feel confident about investing and our learning hub is a good place to start – wherever you are on your journey.