Buy and Hold vs Rebalancing - What is better?

When it comes to building long-term wealth, investors often fall into two camps: those who prefer to buy and hold, and those who favour periodic rebalancing. The first strategy relies on patience and simplicity, the other on discipline and adaptability.

JioBlackRock advantage

·

Published on 20 May 2026

·

4 min read

What does buy and hold really mean?

Advantages of buy and hold:

- Simple to implement and follow.

- Shields you from short-term market noise.

- Minimises transaction costs.

However, buy and hold comes with hidden risks. Over time, outperforming or underperforming assets can skew your portfolio away from its original allocation. For example, a small-cap stock surge may make you overweight in equities. Or inflation might quietly erode the value of your investment in fixed deposits. These scenarios can expose you to more risk than you signed up for. If markets fall, the impact of this portfolio drift can be severe.

What is rebalancing?

Advantages of rebalancing:

- Maintains the portfolio in line with your risk tolerance.

- Prevents overexposure to any one asset class.

- Reduces portfolio volatility over time.

Ensures your portfolio remains on track to help meet your financial objectives.

Rebalancing can be done on a periodic basis say, quarterly or annually or in response to a trigger, such as when asset weights drift beyond a set threshold. Even indices like the NIFTY 50 rebalance every six months, replacing under performers with better performing stocks.

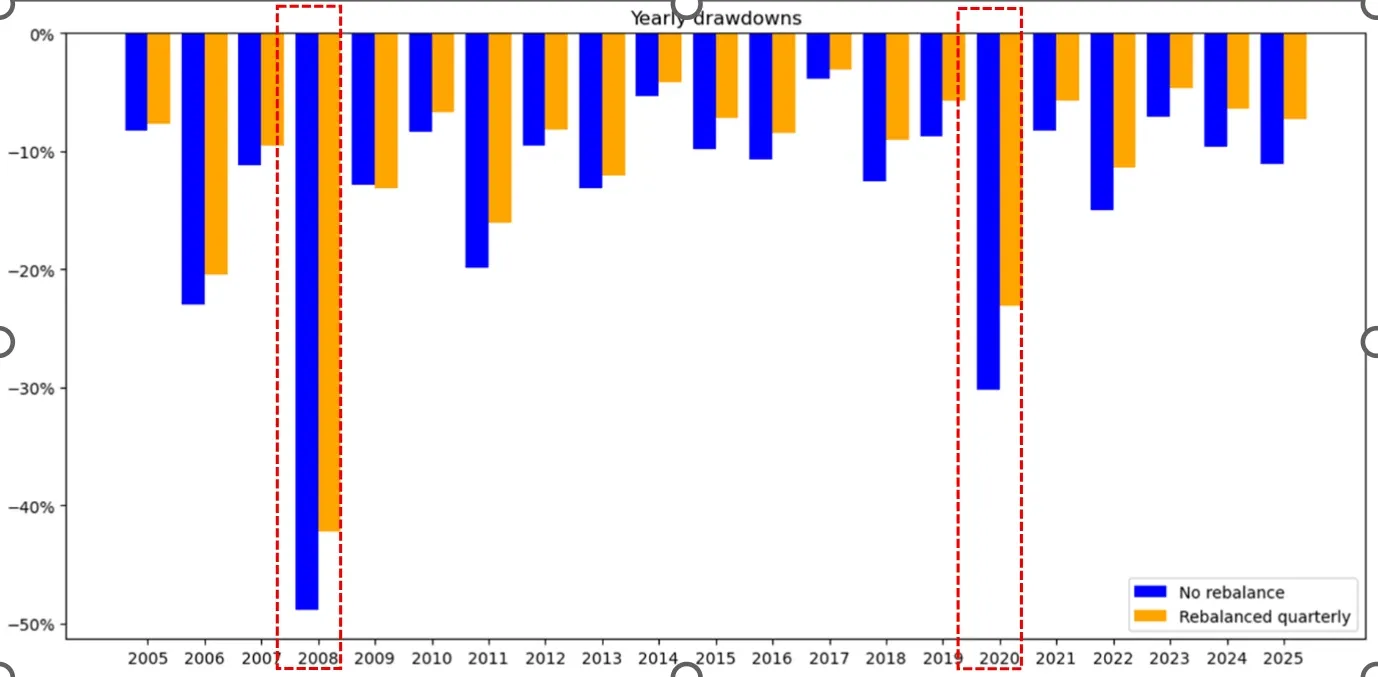

Case study: 2008 and 2020 market volatility

- Portfolio A: Buy-and-hold portfolio i.e. no rebalance (blue bars)

- Portfolio B: Portfolio rebalanced quarterly (orange bars)

During the 2008 global financial crisis:

- Portfolio A dropped 50% from its then high.

- By contrast, Portfolio B retained more value, dropping 42% from its then high.

During the 2020 Covid crash:

- Portfolio A fell by 30% from its immediate high.

- Portfolio B was more resilient and fell only by 23% from its immediate high

Source: Bloomberg. Data as of 30th June, 2025

For illustration purpose only

The above chart shows that most of the time, portfolios that are not periodically rebalanced lose more value than those that are during volatile periods. Rebalancing, therefore, provides a cushion against capital loss. It offers greater resilience and adaptability than buy and hold, especially during market movements, by protecting against drift and sharp downturns. If investors need to withdraw money during a volatile period, they would suffer more losses by withdrawing from un-rebalanced portfolios than rebalanced portfolios.

Key considerations when deciding your portfolio strategy

- Start by assessing your personal comfort level with market volatility by taking a risk profile assessment. If a 30% drop for instance would trigger panic-selling, buy and hold may not be suitable. In such cases, rebalancing provides a rules-based framework that helps maintain discipline and keeps you invested during turbulent times.

- For those in or about to enter retirement, prioritising rebalancing is also important for risk control. Allowing a portfolio to drift to, for example, 80-90% equity exposure just before or during retirement can have negative effects. For this group, a disciplined rebalancing strategy is recommended to preserve capital.

Bottom line: Investing isn’t just about growth, but about risk-adjusted growth

Questions you might have

This article is for educational purpose only.

Blogs

We want everyone to feel confident about investing and our learning hub is a good place to start – wherever you are on your journey.

Monthly Investment Outlook - June 2026

What’s shaping markets this June? The JioBlackRock Investment Team shares its monthly investment outlook for June 2026, discussing the recent market pullback, the impact of geopolitical developments and oil prices on investor sentiment, and our latest asset allocation views. Explore our perspectives on markets, the economy, and opportunities across equities and fixed income.

Why investors need an investment plan not just stock picks

Stock picking might feel right, but without a bigger plan, it’s like sailing without a map. What if the real secret to long-term success isn’t the next hot stock, but a strategy that aligns your money with your life? Discover why an investment strategy beats stock picking every time.

How to interpret returns: Making sense of investment numbers for you

In this article we’ll break down the most common types of investment returns in simple language. By the end, you’ll know exactly what the numbers mean and how to use them.

Why is asset allocation important during periods of market stress?

Equities fuel growth, fixed income provides stability, and gold offers downside protection in uncertain times. Each asset class performs differently under varying market conditions, so what does this mean for you? Read to know….

Monthly Investment Outlook - May 2026

What’s shaping markets this May? The JioBlackRock Investment Team shares monthly investment outlook for May 2026, explaining recent market movements and how portfolios are being positioned today. Explore our latest market views and asset allocation insights.

How we manage risk at JioBlackRock

Long-term investment plans need two things to be successful: alignment to your investment objectives and managing risk at every stage. Risk management begins before you invest and continues throughout the life of your investments. In this article, let us understand how JioBlackRock builds risk management into every stage of your investment journey.