Monthly Investment Outlook - June 2026

What’s shaping markets this June? The JioBlackRock Investment Team shares its monthly investment outlook for June 2026, discussing the recent market pullback, the impact of geopolitical developments and oil prices on investor sentiment, and our latest asset allocation views. Explore our perspectives on markets, the economy, and opportunities across equities and fixed income.

JioBlackRock advantage

·

Published on 11 June 2026

·

2 min read

Market Review

The earnings performance of NSE500 companies for March 2026 quarter has been resilient, but with divergence across market capitalisations and sectors. Large‑cap earnings growth remained in the mid‑single to low‑double‑digit range, though momentum was more muted in globally exposed sectors such as IT services and select metals and energy‑linked companies. In contrast, parts of the mid‑cap universe continued to deliver stronger double‑digit profit growth, on back of resilient domestic demand. Small‑cap results were more mixed, with higher dispersion as input‑cost pressures and tighter financing conditions weighed on profit margins. Sectorally, domestic cyclicals and investment‑linked segments showed stronger earnings momentum, while export‑oriented and commodity‑sensitive sectors experienced greater variability amid currency volatility and elevated energy prices. While headline results largely met expectations, management commentary for the quarter ahead turned cautious, particularly on input cost pressures. Analyst revisions to earnings forecast so far have been benign with FY2027 earnings lower between 1-3% for different market caps and FY2028 earnings largely unchanged. Risks clearly remain to the downside as the full impact of West Asia war will get reflected in inflation and domestic demand in next quarter or so.

On the macro front, the Reserve Bank of India’s Monetary Policy Committee kept the policy repo rate unchanged at 5.25% in its June meeting and retained a neutral stance, with a more cautious tone. The RBI revised its FY27 GDP growth forecast to 6.6% (from 6.9%) and raised its inflation projection to 5.1% (from 4.6%), citing risks from elevated crude oil prices, geopolitical tensions in West Asia, supply‑chain disruptions, and currency pressures. The central bank also announced various measures aimed at supporting external stability and attracting foreign capital. India’s growth data remained resilient despite the challenging global backdrop. The economy expanded 7.8% YoY in Q4 FY26, taking full‑year GDP growth for FY26 to 7.7%, supported by strength in services, construction, and investment‑linked sectors, even as higher commodity prices and external uncertainty began to weigh on parts of manufacturing.

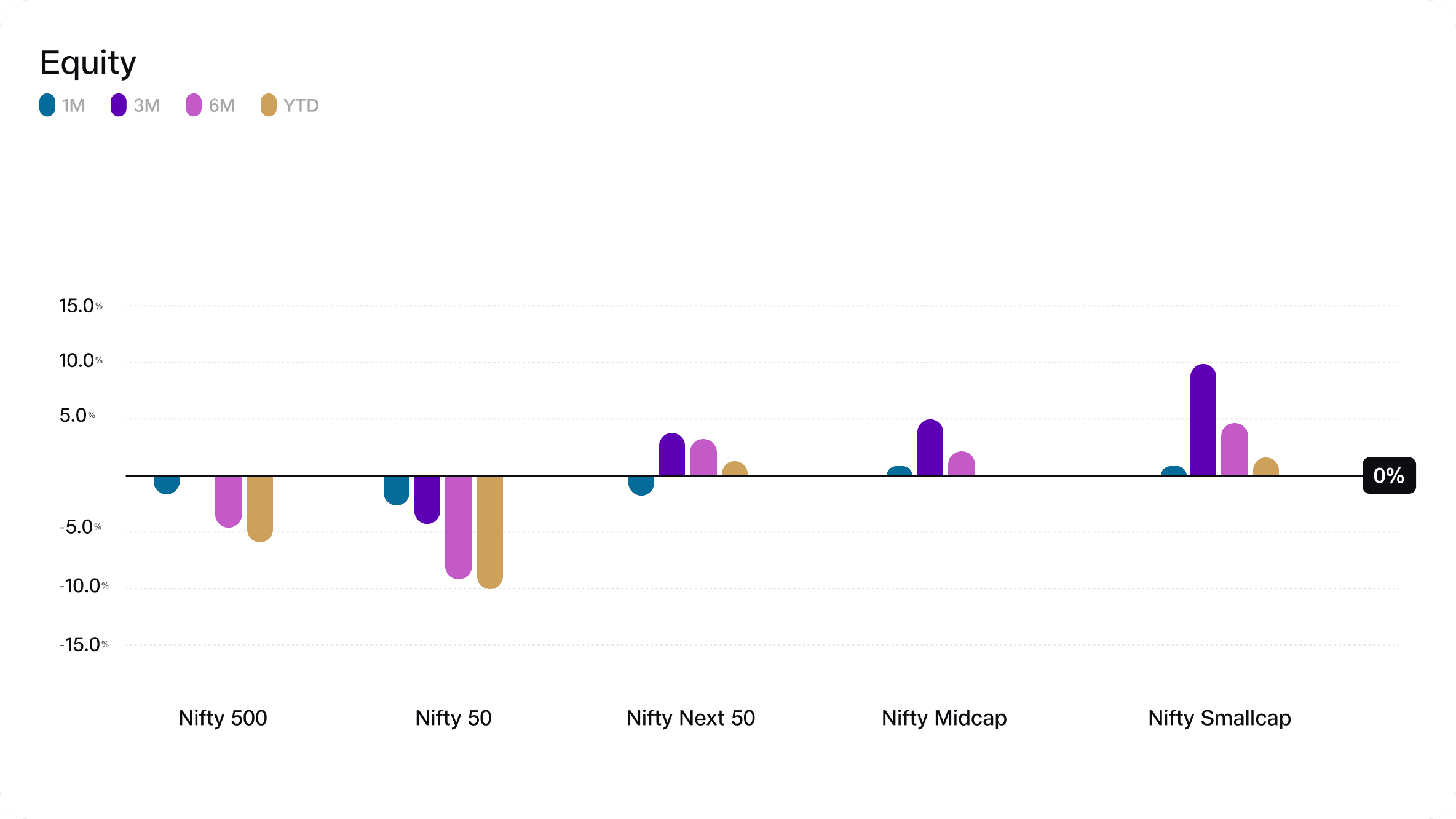

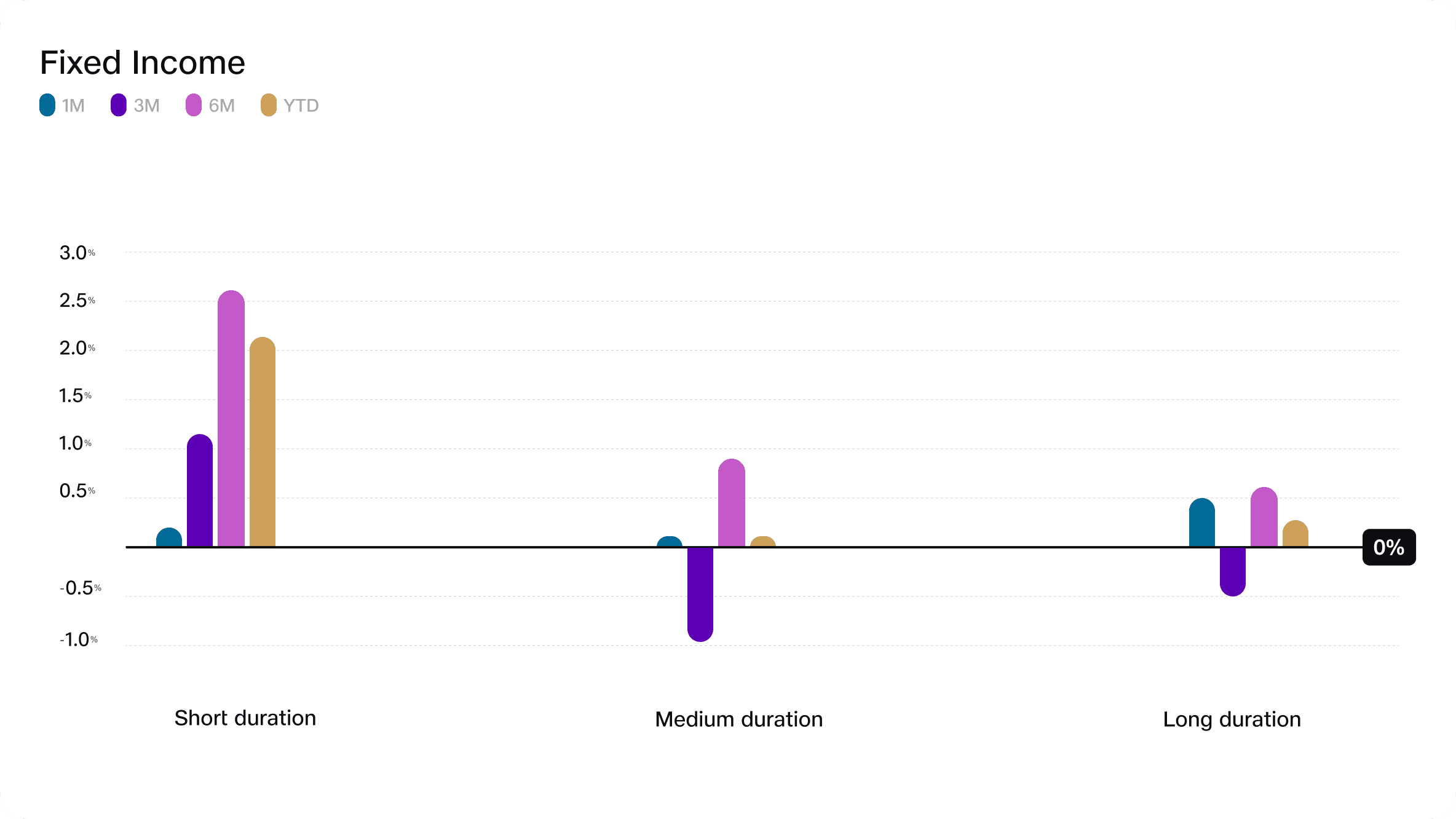

Market Performance

Source: Bloomberg,

Data: As of 4th June 2026

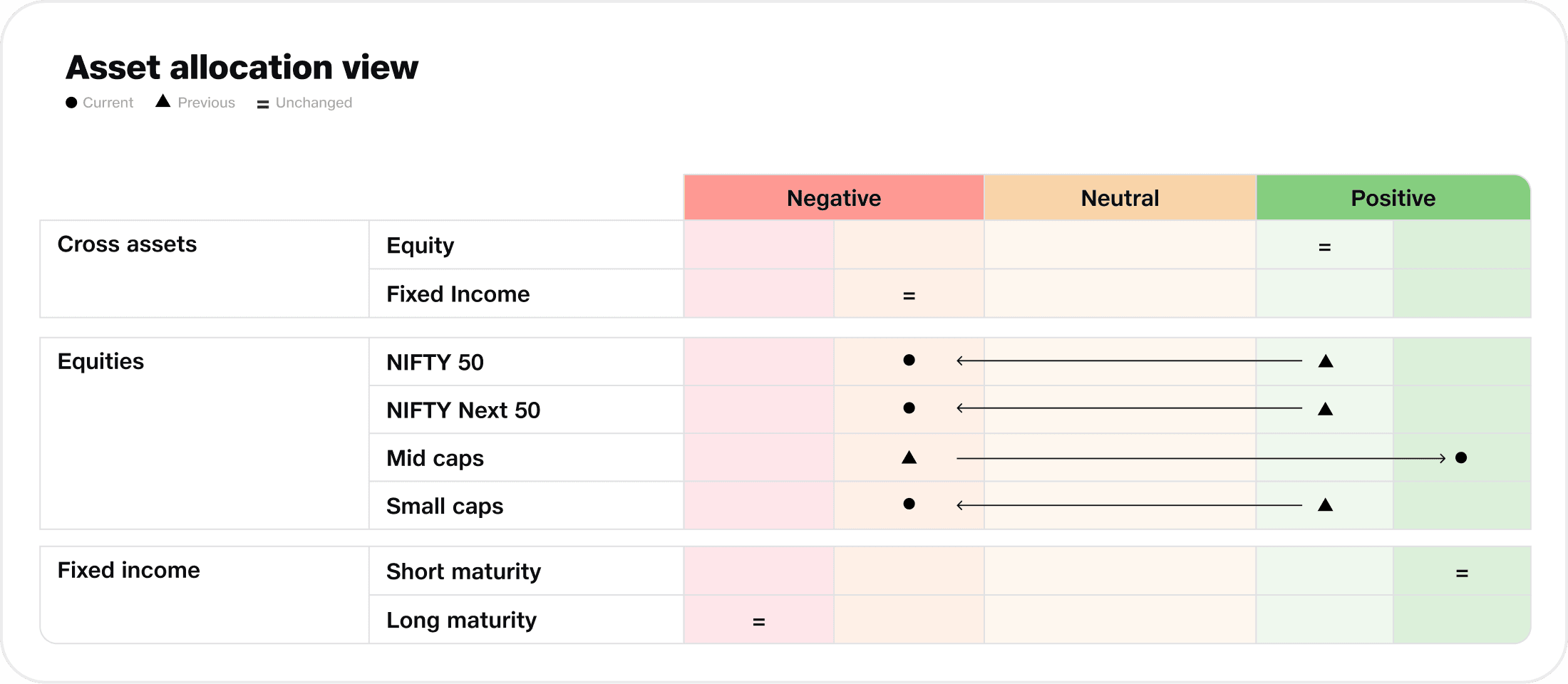

Last month, we had taken a risk management step despite a positive stance on equities. When tail risks rise, we reduce the extent of under or overweight on different asset classes which our signals highlight to us. This approach was applied as the West Asia conflict persisted longer than expected, keeping uncertainty around oil prices, the currency, and global sentiment elevated. The objective was not to change our constructive view on equities, but to protect portfolios during a period when adverse scenarios carried higher near‑term impact. Over the past month, the tail risks have decreased as US-Iran diplomatic talks towards a resolution have moved ahead. Whilst a deal is still to be finalised, the actions of both parties have reduced the likelihood of extreme escalation and markets have graduated to this scenario. While geopolitical risks have not fully disappeared, the balance has shifted away from tail‑risk outcomes toward a more manageable range of potential developments. Additionally recent policy actions from RBI and the government to attract foreign capital have also helped stabilise USDINR which was becoming a cause of worry for India.

Given the improved risk scenario and our signals still positive on equities, our asset allocation changes are reflected above. The fundamental drivers supporting equities have remained intact. Earnings trends continue to be resilient, domestic growth conditions remain supportive, and relative valuations in parts of the market have improved following recent consolidation.

Within equities, our relative preference has changed towards mid-caps versus the earlier preference for large and small-caps. Mid‑cap companies continue to deliver strong earnings growth, and importantly earnings estimates for mid-caps have begun to improve meaningfully.

Within fixed income, our preference for shorter‑maturity investments remains unchanged. While the RBI continues to maintain a supportive stance on liquidity and has kept policy rates steady, longer‑term bond yields remain sensitive to inflation expectations, currency volatility, and fiscal concerns amid elevated energy prices. As a result, longer‑duration bonds have seen periodic upward pressure on yields and higher price volatility. In contrast, shorter‑maturity instruments have remained more stable and continue to offer a better balance between income and capital stability.

Thank you for reading our June 2026 Investment Outlook. We look forward to sharing our latest market perspectives with you again next month.

Disclaimers

This Commentary is for limited distribution only and the recipient shall not copy/circulate/reproduce/quote contents of this document, in part or in whole, or in any other manner without prior and explicit approval of JBIAPL and treat the information contained in this Commentary with utmost confidentiality. The information is only for consumption by the client/recipient and such material should not be redistributed. If you are not the intended recipient, you are hereby notified that any use, distribution, reproduction, or any action taken or omitted to be taken in reliance of the same is strictly prohibited and may be unlawful.

This Commentary contains information, data, charts, and materials obtained from external and third-party sources ("Third-Party Information"). While JBIAPL believes such Third-Party Information to be reliable, JBIAPL has not independently verified such information and makes no representation or warranty as to its accuracy, completeness, or timeliness. JBIAPL assumes no liability for any errors, omissions, or inaccuracies in such Third-Party Information.

This Commentary is provided "as is" for informational and discussion purposes only. JBIAPL makes no representation or warranties, express or implied, regarding:

- The accuracy, completeness, or reliability of the information contained herein;

- The profile or data points of any underlying issuers, products or services;

- The suitability of any information for any particular purpose;

- Any outcomes or results that may be achieved.

Nothing in this Commentary constitutes legal, financial, investment, tax, professional advice or an investment advice, research report, or a recommendation or a solicitation to invest in any financial product or security or entity, or a promotion of any such financial product or security or entity, in any manner whatsoever or recommendation by JBIAPL of an investment strategy or whether or not to "buy", "sell" or "hold" an investment. The information available in this Commentary should not be considered as sufficient upon which to base an investment decision and is not based on consideration of the recipient's individual circumstances. Recipients should consult their own advisors before making any decisions based on information contained herein. This Commentary contains certain assumptions and views, which JBIAPL considers reasonable at this point in time, and which are subject to change. The views set out in this Commentary are indicative and are based on current market prices and general market sentiment.

All intellectual property rights in this Commentary, including but not limited to copyrights, trademarks, trade secrets, and proprietary information, remain the exclusive property of the JBIAPL or its licensors. No license or right is granted except as expressly stated herein.

To the fullest extent permitted by law, JBIAPL shall not be liable for any damages, losses, costs, or expenses arising from or relating to the use of, reliance upon, or inability to use the information contained in this Commentary.

Blogs

We want everyone to feel confident about investing and our learning hub is a good place to start – wherever you are on your journey.

Monthly Investment Outlook - July 2026

What’s shaping markets this July? The JioBlackRock Investment Team shares its monthly investment outlook for July 2026, explaining recent market sentiments and how portfolios are being positioned today. Explore our latest market views and asset allocation insights.

How to interpret returns: Making sense of investment numbers for you

In this article we’ll break down the most common types of investment returns in simple language. By the end, you’ll know exactly what the numbers mean and how to use them.

Buy and Hold vs Rebalancing - What is better?

When it comes to building long-term wealth, investors often fall into two camps: those who prefer to buy and hold, and those who favour periodic rebalancing. The first strategy relies on patience and simplicity, the other on discipline and adaptability.

Why is asset allocation important during periods of market stress?

Equities fuel growth, fixed income provides stability, and gold offers downside protection in uncertain times. Each asset class performs differently under varying market conditions, so what does this mean for you? Read to know….

Why investors need an investment plan not just stock picks

Stock picking might feel right, but without a bigger plan, it’s like sailing without a map. What if the real secret to long-term success isn’t the next hot stock, but a strategy that aligns your money with your life? Discover why an investment strategy beats stock picking every time.

Monthly Investment Outlook - May 2026

What’s shaping markets this May? The JioBlackRock Investment Team shares monthly investment outlook for May 2026, explaining recent market movements and how portfolios are being positioned today. Explore our latest market views and asset allocation insights.